From Credit Card to Mortgage: Building U.S. Credit Toward a Home Loan

How a credit card and a mortgage differ, how each charges interest, and how building credit-card history (even with an ITIN, no SSN) leads to a home loan.

Svetlana Burninova

CTO & Co-Founder

A credit card and a mortgage are the two debts you will deal with most in the United States, and they work in almost opposite ways. A credit card is unsecured, revolving, and expensive, but it is also how you build the credit history a mortgage lender needs to see. A mortgage is secured, scheduled, and comparatively cheap. You can even get one with an ITIN and no Social Security Number. This guide walks the path from one to the other.

Most people arriving in the U.S. are told two things that sound contradictory: "avoid debt," and "you need credit to get anywhere." Both are true. The way to hold them together is to understand that not all debt is the same, and that responsible use of a credit card is what eventually unlocks a home loan.

The two debts you will deal with most

U.S. consumer debt splits two ways. Secured debt is backed by something the lender can take if you stop paying, like your house or your car. Unsecured debt is backed only by your promise to repay. Separately, debt is either installment (you borrow a fixed amount once and pay it down on a schedule) or revolving (you have a limit you can borrow, repay, and borrow again).

A mortgage is secured and installment. A credit card is unsecured and revolving. That single distinction drives everything else.

A credit card:

A mortgage:

The credit card looks like the small debt and the mortgage like the big one. But the small one is usually the expensive one, and it is the one that decides whether you ever qualify for the big one.

How interest really works on each

This is the difference that costs people the most money, and almost nobody explains it plainly.

A mortgage charges simple interest on a shrinking balance, and you cannot avoid it. Interest is calculated on the principal you still owe and built into a fixed monthly payment, an "amortization schedule." Early on, most of your payment is interest; later, most of it is principal, even though the payment amount stays the same. It accrues from day one, but the rate is low.

A credit card compounds interest daily, but only if you carry a balance. The card has a grace period: if you pay your full statement balance by the due date, you pay zero interest on new purchases. Carry even part of the balance and you lose that grace period. Interest is then charged daily on your average balance, and it starts accruing on new purchases from the day you make them. At around 22% APR, that daily compounding adds up fast.

So the rule for newcomers is simple and powerful: use the credit card every month, and pay it in full every month. You build credit history and pay nothing for it. The moment you carry a balance, the card flips from a free credit-building tool into your most expensive debt.

Which one to pay down first

If you ever carry both, pay the credit card first. It is almost always the higher rate, and paying it down also lowers your credit utilization, how much of your limit you are using, which is one of the biggest factors in your score. Mortgages are large, long, and cheap, so they sit last on the payoff list. Paying the highest rate first is called the avalanche method, and you can compare it to the snowball method in our guide to debt snowball vs debt avalanche.

How a credit card builds the credit a mortgage needs

A mortgage lender wants to see that you have borrowed before and repaid reliably. With no U.S. history, you start at zero, and a credit card is the most common way to build from there. The factors that move your score:

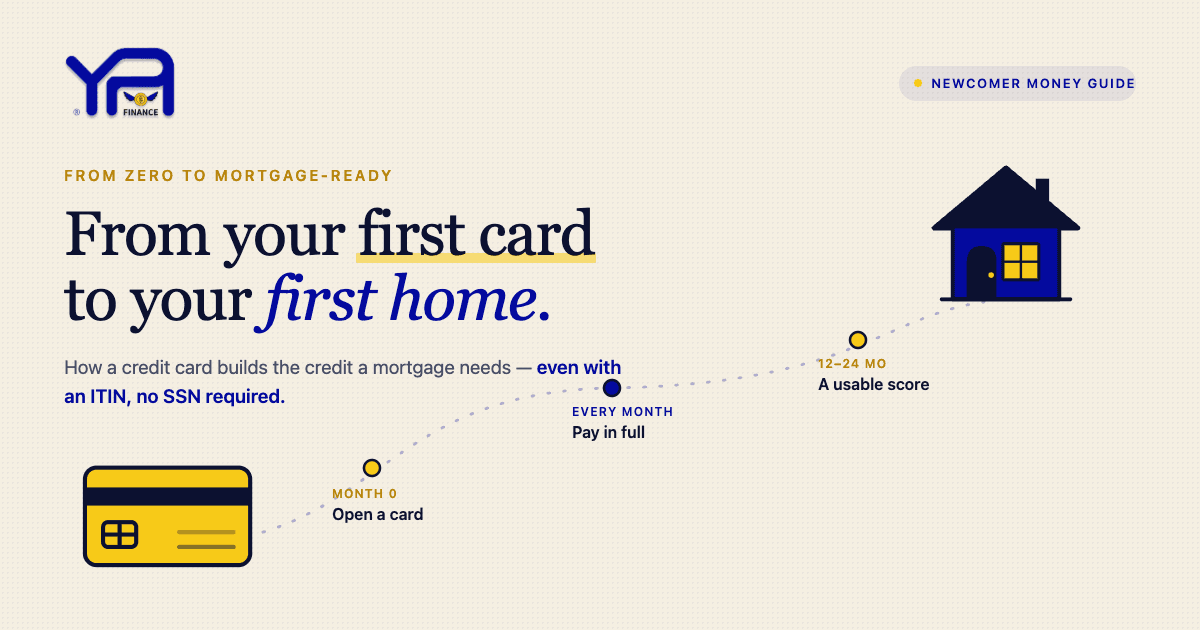

If you do not qualify for a regular card yet, a secured card (you put down a refundable deposit that becomes your limit) or a credit-builder loan does the same job, and both report to the credit bureaus. With some lenders and services, on-time rent and utility payments can also count as alternative data. A FICO score usually needs about six months of reporting before it appears at all, then strengthens over a year or two of steady use. For the full step-by-step, see how to build credit from zero and our complete credit score guide for immigrants.

Buying a home without an SSN: the ITIN path

Here is what most guides will not tell you clearly: you do not need a Social Security Number to get a mortgage. Lenders who offer ITIN mortgages accept an Individual Taxpayer Identification Number instead. Terms vary by lender, and these are typical rather than guaranteed:

That history is exactly what your credit card has been building. The ITIN mortgage is not a separate, mysterious product. It is the same destination reached by the same road, credit built one paid-in-full statement at a time. To prepare the credit, savings, and documents that get you there, see how to get financially ready to buy a home.

A realistic timeline from zero to mortgage-ready

It is not fast, but it is a known path, and every step is something you control.

Common questions

Do I need a credit card before I can get a mortgage?

Not literally, but you need a credit history, and a credit card is the most common way to build one. A mortgage lender wants evidence that you have borrowed and repaid reliably.

Can I get a mortgage without a Social Security Number?

Yes. ITIN mortgages let you use an Individual Taxpayer Identification Number instead of an SSN, usually with a larger down payment (often around 10 to 20%) and a higher rate, offered mainly by credit unions and community lenders.

Can I avoid paying interest on a credit card?

Yes, on new purchases, if you pay your full statement balance by the due date each month. Carry a balance and you lose that grace period, and interest starts accruing daily.

Should I pay off my credit card or my mortgage first?

The credit card, in almost every case. It usually has a much higher rate, and paying it down also lowers your credit utilization, which helps your score.

Why is credit card interest so much higher than a mortgage's?

A mortgage is secured by your home, so the lender's risk is lower. A credit card is unsecured, so the rate is higher to offset that risk.

How long does it take to build credit for a mortgage?

A score usually appears after about six months of reporting, then grows strong over a year or two of steady, on-time activity. Qualifying for a specific loan also depends on your income, down payment, and the lender.

YPA-FINANCE helps immigrants and newcomers understand credit score, budgeting, and debt payoff in 13+ languages, with simple tools, plain language, and support that feels human.