Mayroon akong 3 credit card at hindi ko na kaya — Saan magsisimula?

Ang pamamahala ng maraming credit card ay parang juggling. Narito ang eksaktong tatlong-hakbang na plano para lumipat mula sa kaguluhan tungo sa kalinawan — at simulan ang tamang pagbabayad ng utang.

Svetlana Burninova

CTO & Co-Founder

Nagsisimula ito nang walang kasalanan.

Isang card para sa pang-araw-araw na gastos. Isa para sa biglaang pagkukumpuni ng sasakyan. Marahil isang ikatlo dahil sinabi ng isang tao sa bangko na sulit ang mga reward.

Ngunit bigla na lang, hindi ka na namamahala ng credit — nagju-juggle ka na. Magkakaibang petsa ng bayad. Magkakaibang interest rate. Ang patuloy na takot na ang isang napalampas na bayad ay magwawasak sa lahat ng iyong pinagsikapang itayo.

Naririnig ko ito mula sa mga gumagamit ng YPA nang paulit-ulit. At ang unang bagay na sinasabi ko sa kanila ay katulad ng gusto kong sabihin ng isang tao sa aking kapatid nang lumipat siya sa Estados Unidos: ang kalituhan na nararamdaman mo ay hindi personal na kabiguan. Ito ang nangyayari kapag ang isang kumplikadong sistema ay hindi nagbibigay sa iyo ng anumang manwal.

Narito ang manwal na hindi mo natanggap.

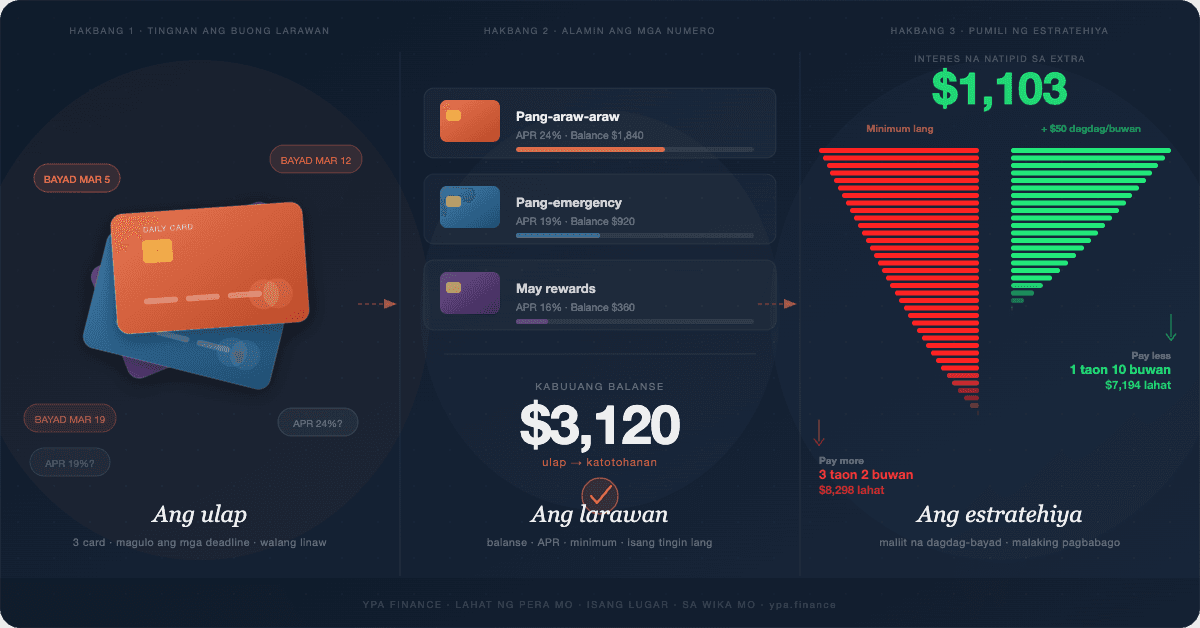

Hakbang 1: Bago pa man — tingnan ang buong larawan

Iniiwasan ng karamihang tao ang hakbang na ito hindi dahil mahirap kundi dahil hindi komportable. Ang makita ang bawat balanse sa isang lugar ay maaaring makaramdam na parang sumakay ka na sa timbangan pagkatapos ng maraming buwang pag-iwas.

Gawin mo pa rin.

Ilista ang bawat card na may balanse. Para sa bawat isa, isulat ang tatlong numero:

Iyon lang. Wala pang matematika.

Bakit ito mahalaga: ngayon ang iyong utang ay parang hamog — maraming bayad, nakakalat na petsa, isang numero na mas gusto mong huwag pag-isipan. Ang pagsulat nito ay nagbabago ng hamog sa katotohanan. At ang katotohanan ay maaaring harapin.

Isang hindi inaasahang bagay ang karaniwang nangyayari sa hakbang na ito: ang sitwasyon ay parang hindi na gaanong nakakapruweba. Hindi dahil nagbago ang mga numero — kundi dahil ngayon ay malinaw mo na silang makikita.

Hakbang 2: Pumili ng estratehiya at unawain kung bakit ito gumagana

Kapag alam mo na ang iyong kinakaharap, ang tanong ay: aling card ang uunahing harapin?

Dalawang estratehiya ang nakatulong sa milyun-milyon na makalabas sa utang. Wala sa dalawa ang mali. Ang tama ay ang talagang mananatili ka.

Ang Debt Snowball — para sa kapag kailangan mo ng momentum

Bayaran ang minimum sa lahat. Ilagay ang bawat karagdagang piso sa pinakamaliit na balanse. Kapag natapos na, ilipat ang bayad na iyon sa susunod na pinakamaliit.

Ang matematika ay hindi perpekto. Ngunit ang sikolohiya ay oo. Ang Snowball ay nagbibigay ng iyong unang tagumpay na walang utang sa ika-3 buwan — ang Avalanche ay hindi nakakaabot sa una nito hanggang sa ika-7 buwan. Para sa maraming tao, ang apat na buwang pagkakaiba ay kung saan nagtatagumpay o nabibigo ang mga plano.

Ang Debt Avalanche — para sa kapag gusto mong mabawasan ang interes

Bayaran ang minimum sa lahat. Ilagay ang bawat karagdagang piso sa card na may pinakamataas na APR muna. Magtrabaho pababa mula doon.

Ang Avalanche ay karaniwang nakakatipid ng pinakamarami sa interes, lalo na kapag mayroon kang mga utang na may malawak na hanay ng mga interest rate. Kung may disiplina ka at motivated ka sa pamamagitan ng mga numero, ito ang mas mahusay na landas.

Alin ang pipiliin?

Kung hindi ka sigurado — magsimula sa isang maliit na tagumpay. Bayaran ang pinakamaliit na balanse. Tingnan kung ano ang pakiramdam ng zero. Ang pakiramdam na iyon ay data. Sasabihin nito sa iyo kung ikaw ay Snowball o Avalanche na tao.

Hindi sigurado kung aling estratehiya ang nakakatipid ng mas marami sa iyong mga partikular na card? I-plug ang iyong mga balanse at APR sa Calculator PRO — kinakalkula nito ang mga numero para sa parehong estratehiya at ipinapakita sa iyo nang eksakto kung magkano ang matitipid mo sa interes at kung gaano katagal ang pagbabayad.

Hakbang 3: Alisin ang alitan

Narito ang pumapatay sa karamihang plano sa pagbabayad ng utang: hindi kawalan ng motibasyon, kundi kawalan ng sistema.

Magkakaibang app para sa magkakaibang card. Mental arithmetic para masubaybayan ang progreso. Mga petsa ng bayad na hindi magkatugma. Ang bawat karagdagang alitan ay isang dahilan para mawalan ng track.

Sa YPA Finance, binuo namin ang tracking layer partikular dahil ang aming mga gumagamit — marami sa kanila ay mga immigrant na namamahala ng pananalapi sa isang bagong bansa, sa isang pangalawang wika, nang walang sinuman na matatawagan para sa payo — ay hindi kayang mapalampas ang track. Isang dashboard. Bawat card. Real-time na mga update ng balanse habang sumusulong ka. Mga paliwanag sa simpleng wika ng nangyayari at kung ano ang gagawin sa susunod.

Dahil ang paglabas sa utang ay hindi lang matematika. Ito ay isang sistema na kailangan mong masundan kapag abala ang buhay.

Ang konklusyon

Hindi mo kailangan ng mas maraming lakas ng kalooban. Kailangan mo ng mas malinaw na larawan, isang estratehiya na akma sa paraan ng pag-iisip ng iyong utak, at isang sistema na nag-aalis ng alitan sa pagitan mo at ng plano.

Ang tatlong card na ngayon ay nakakapruweba ay isang problemang may solusyon. Kailangan mo lang ng manwal.

---

Si Svetlana Burninova ay co-founder at CTO ng YPA Finance, isang multilingual personal finance platform na itinayo para sa mga immigrant na nagna-navigate sa sistemang pinansyal ng Estados Unidos. Magsimula dito →

Mga kaugnay na artikulo

Debt snowball o avalanche: aling paraan ng pagbabayad ang talagang gumagana?

8 minuto basahin

Credit CardsNakuha Ko ang Unang Credit Card Ko sa U.S. at Natuto Ako sa Masakit na Paraan

9 min na pagbasa

BudgetingKung Paano Ang Mga Imigrante at Unang Henerasyon na Pamilya Ay Maaaring Gamitin ang 50/30/20 Budget Rule

8 min na pagbasa