How to Pay Off Credit Card Debt Fast: A 5-Step Plan

Paying off credit card debt fast isn't about earning more, it's about attacking the balance, not the interest. Here's the exact 5-step plan, with a free calculator to see your finish line.

Svetlana Burninova

CTO & Co-Founder

The minimum payment is a trap dressed up as responsibility. You pay it on time, every month, and it feels like progress, but most of it goes to interest, and the balance barely moves.

That is by design. The minimum payment is set to keep you in debt as long as legally possible. A $3,000 balance at 24% APR, paid at the minimum, can take over 15 years to clear and cost more than the original balance again in interest.

Paying off credit card debt fast is not about earning more money. It is about changing the order and the size of your payments so that more of each dollar attacks the balance instead of the interest. When we built the debt tools inside YPA Finance, this is the approach we built them around, and it is what the numbers below will show you.

Why credit card debt grows so fast

Credit cards charge compound interest, usually calculated daily. Your APR (annual percentage rate) is divided by 365 to get a daily rate, and that rate is applied to your balance every single day. The interest you were charged yesterday becomes part of the balance that gets charged interest today.

That is why a balance you're "paying down" can feel stuck. If your APR is 24%, you're being charged roughly 2% of your balance in interest every month before you pay a cent toward what you actually borrowed. The minimum payment is usually just that interest plus 1% of the balance, which is why it barely dents the total.

The single most important number to know is your APR. If you're not sure how to find it or what it means, read how credit card interest actually works first, then come back.

Step 1: Stop adding to the balance

You cannot pay off a balance you keep feeding. Before any strategy works, the card has to stop being a spending tool and become a debt you're closing.

Move your everyday spending to a debit card or cash for a few months. This is not forever. It's until the balance is gone. Keep the credit card open (closing it can hurt your credit score by lowering your available credit), just stop using it.

Step 2: Know your real numbers

Write down, for every card: the balance, the APR, and the minimum payment. You cannot make a plan from a vague sense of "a lot." You need the actual figures.

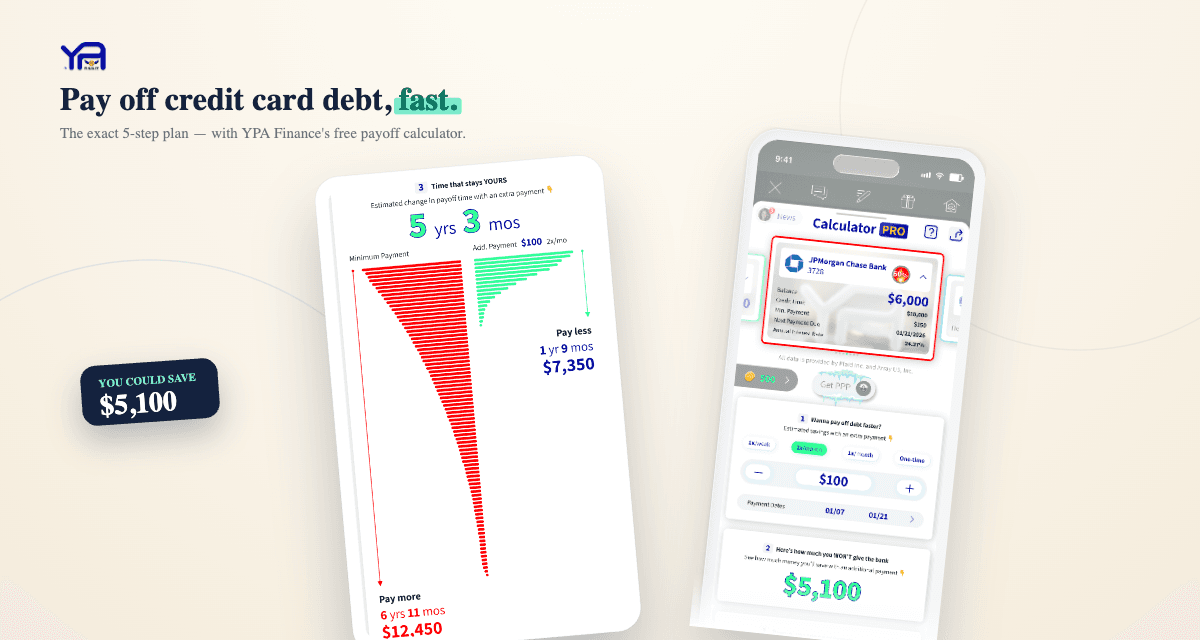

Then find out what those numbers mean over time. Our free Calculator PRO shows you exactly how long your current payment will take, how much interest you'll pay, and, this is the part that changes behavior, how much time and money you save by paying a little more each month. Seeing "you save 4 years and $2,100 by paying $80 more" is more motivating than any budgeting lecture.

Step 3: Pick a payoff strategy

If you have more than one card, the order you pay them in matters. There are two proven methods.

The debt snowball: pay minimums on everything, then throw every extra dollar at the *smallest* balance first. When it's gone, roll that payment into the next-smallest. You get quick wins that keep you motivated.

The debt avalanche: pay minimums on everything, then attack the card with the *highest APR* first. This saves you the most money mathematically, because you're killing your most expensive debt first.

Both work. The snowball keeps you going; the avalanche saves more. I break down the exact math, with examples, in debt snowball vs. debt avalanche. If you're not sure which fits you, start with the snowball, momentum matters more than a few dollars when you're just starting.

Step 4: Find extra money to throw at it

Every dollar above the minimum goes straight to the principal, so finding even small amounts speeds things up dramatically.

A 50/30/20 budget can help you find the "extra" without feeling deprived, it earmarks 20% of income for debt and savings by default.

Step 5: Consider consolidation, carefully

If your credit is decent, two tools can lower the interest working against you:

Neither erases the debt. They just change the terms so you can pay it off faster. Only use them if you've done Step 1, if you keep spending, consolidation just frees up the card to run the balance back up.

How fast can you realistically pay it off?

With a single average balance and a serious plan, a few months to a couple of years is realistic for most people. The variables are your balance, your APR, and how much above the minimum you can pay. The last one is the only one fully in your control, and it's the one that matters most.

Run your own numbers before you start. Knowing the finish line, "18 months if I pay $150," turns a vague dread into a plan you can actually follow.

Frequently asked questions

Is it better to pay off credit card debt or save money first?

Build a small emergency buffer (even $500-1,000) so a surprise doesn't send you back to the card, then focus everything on the debt. Credit card APRs are almost always higher than what a savings account pays, so paying off the card is a guaranteed return you can't beat elsewhere.

Does paying off a credit card help my credit score?

Yes. Paying down balances lowers your credit utilization (how much of your limit you're using), which is one of the biggest factors in your score. Keep the card open after paying it off so your available credit and account age keep helping you.

Should I pay off the card with the highest interest or the smallest balance first?

Highest interest (the avalanche) saves the most money. Smallest balance (the snowball) gives faster wins and keeps you motivated. Both work, the best one is the one you'll actually stick with.

Will paying only the minimum ever clear my debt?

Technically yes, but it can take 15+ years on a typical balance and cost more in interest than you originally borrowed. Paying even a little above the minimum dramatically shortens that timeline.

How much faster do I pay off debt by paying more than the minimum?

Often years faster. Because everything above the minimum goes straight to principal, even an extra $50-100 a month can cut a multi-year payoff down to months. Use a payoff calculator to see your exact numbers.

The bottom line

Fast credit card payoff comes down to five moves: stop adding to the balance, know your real numbers, pick a strategy (snowball or avalanche), throw every extra dollar at the principal, and consider consolidation only if it genuinely lowers your rate. None of it requires earning more. It requires seeing the real cost clearly, then paying with intent instead of on autopilot.

Start by running your balance through the credit card payoff calculator. Once you see your actual finish line, the plan writes itself.